AGEAS-Project

Insurance Claim Modeling with Random Forest

Frequency–Severity Approach

TL;DR

Two-part insurance risk model:

- Frequency → probability of a claim

- Severity → size of a claim

Combining both:

Expected Loss = Frequency × Severity

This project applies Random Forest models to capture nonlinear risk patterns and analyze insurance portfolio behavior.

Problem

Insurance risk is not a single prediction problem.

Instead, expected loss is modeled as:

Expected Cost = Frequency × Severity

Where:

- Frequency = likelihood of a claim

- Severity = cost given a claim

This structure better reflects real-world insurance pricing.

Methodology

Frequency Model

- Random Forest Classifier

- Predicts claim probability

Severity Model

- Random Forest Regressor

- Predicts claim size

Final Output

- Combined into Expected Loss per customer

Key Results

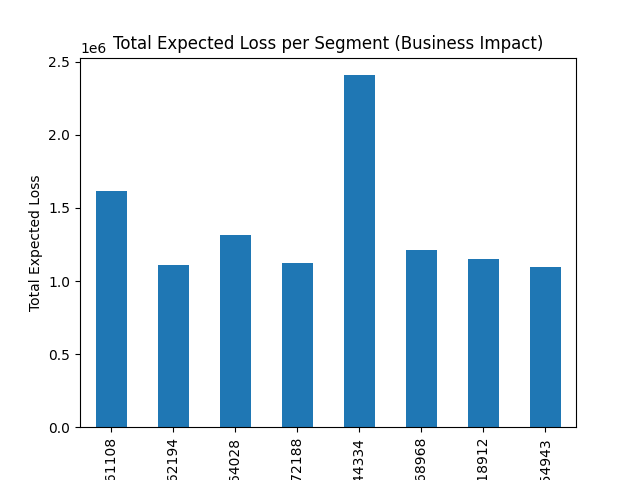

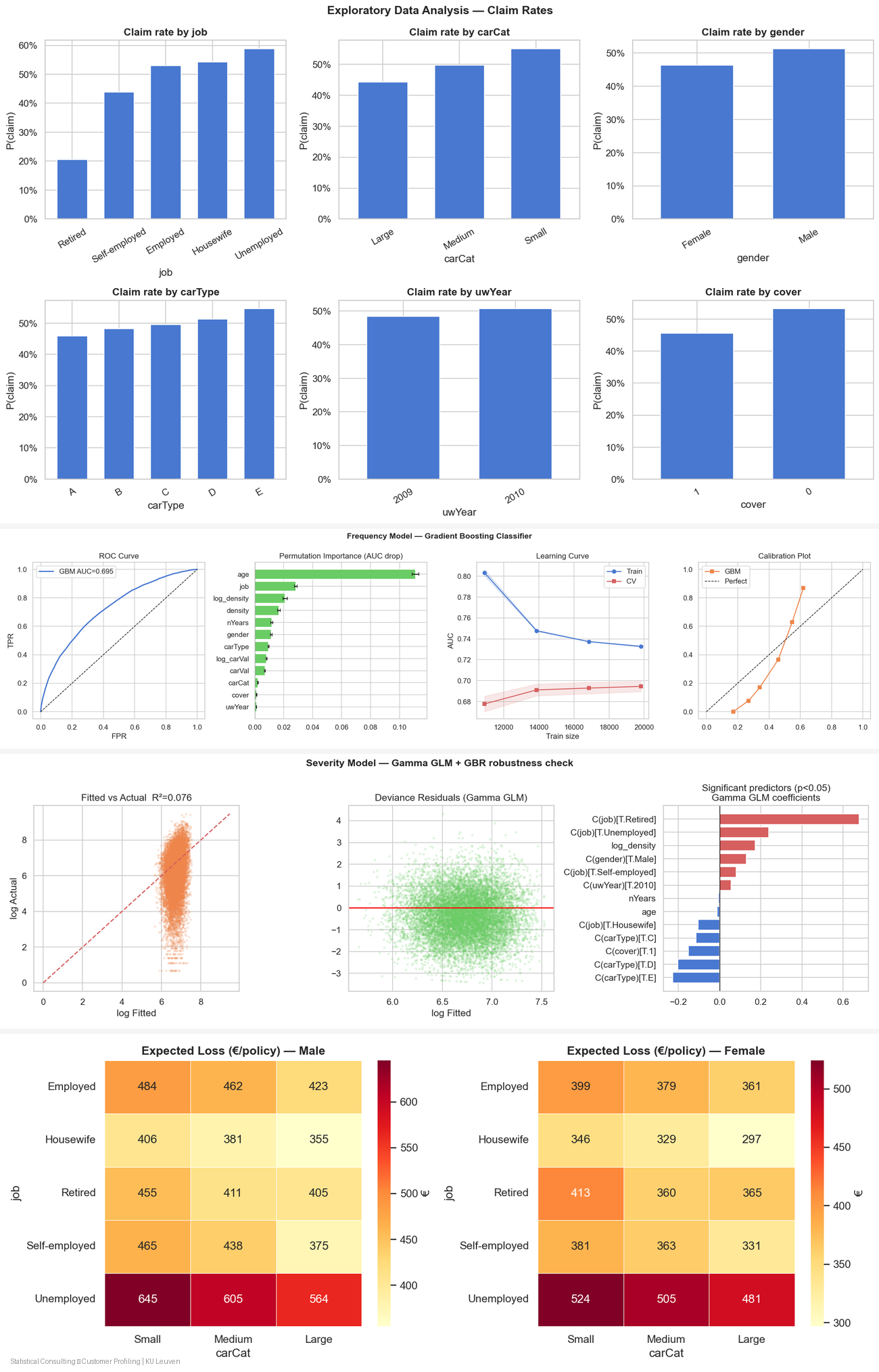

Business Impact: Total Expected Loss per Segment

Some segments contribute disproportionately to total loss.

This highlights that portfolio concentration is as important as individual risk.

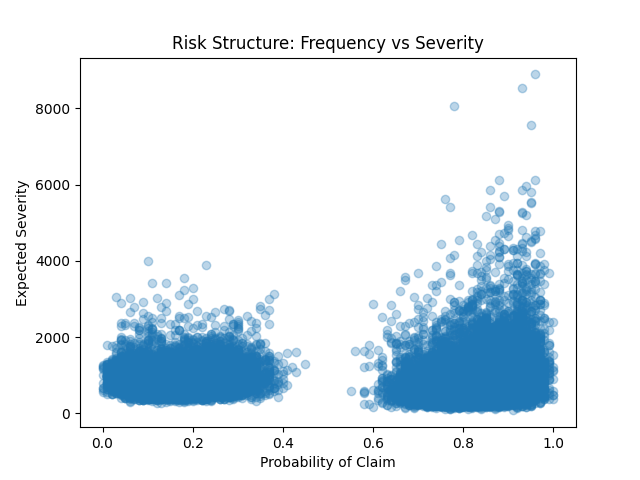

Risk Structure: Frequency vs Severity

There is a clear nonlinear relationship:

- High claim probability often coincides with high severity

- Risk is clustered rather than evenly distributed

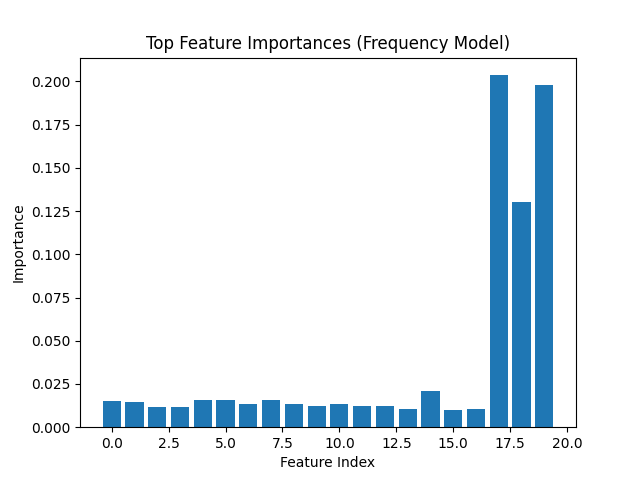

Feature Importance (Frequency Model)

A small number of features dominate prediction power,

suggesting strong underlying drivers of claim occurrence.

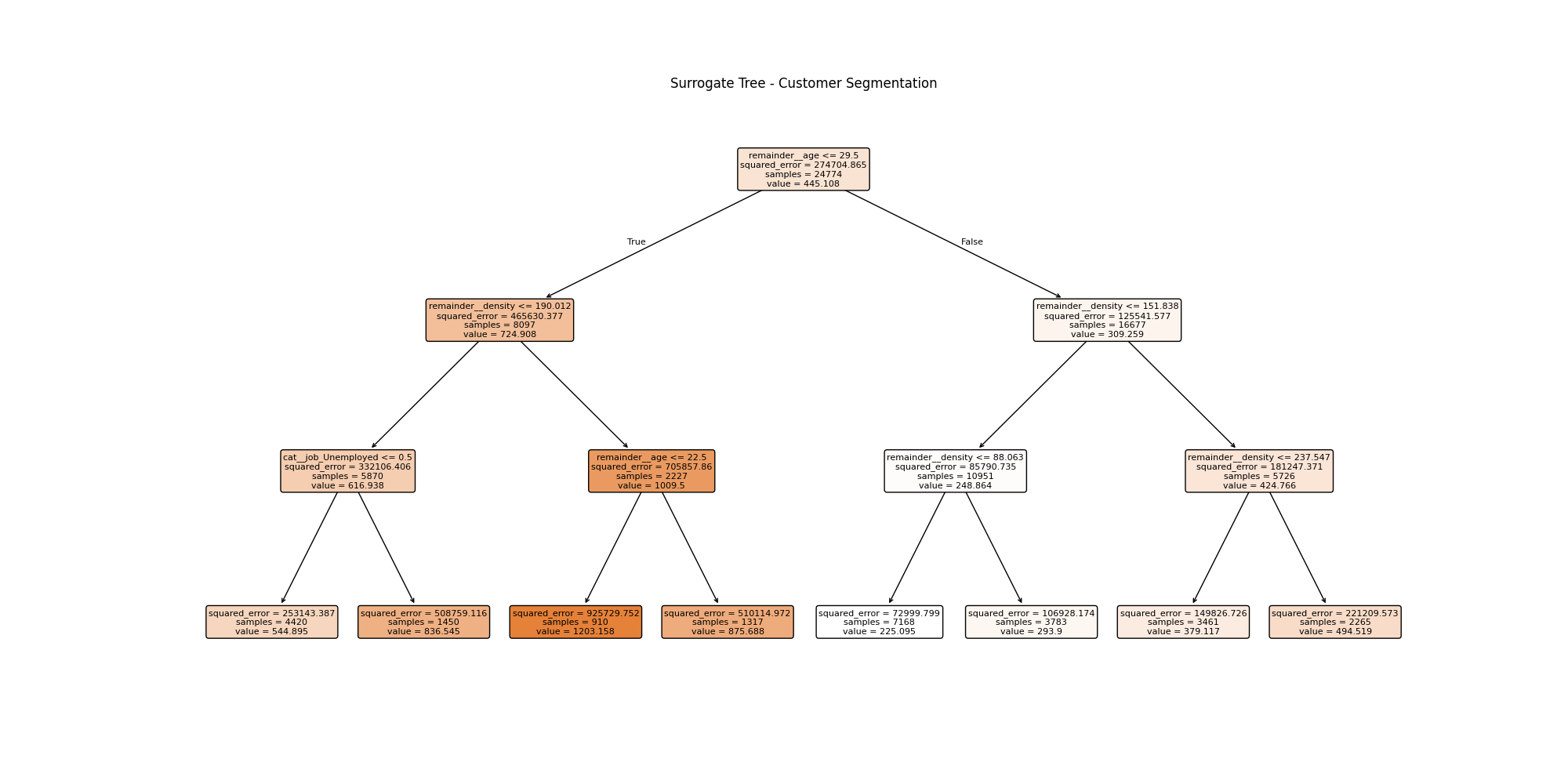

Interpretable Segmentation (Surrogate Tree)

A decision tree approximation of the model reveals:

- Clear segmentation rules

- Key thresholds driving risk differences

- Interpretable structure behind a complex model

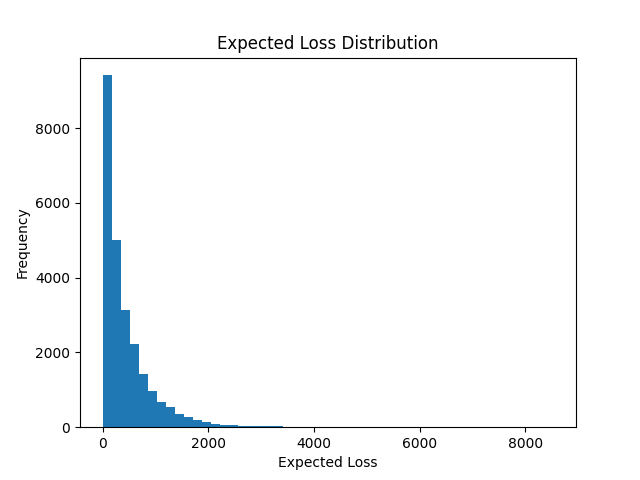

Distribution of Expected Loss

The distribution is highly skewed:

- Most customers have low expected loss

- A small group drives extreme risk

This is typical in insurance and reinforces the need for segmentation.

Portfolio-Level Insights

Customer Segmentation Overview

- High-risk groups are identifiable

- Job category, car type, and demographics affect claim behavior

- Certain segments consistently exhibit elevated expected loss

Key Takeaways

- Modeling frequency and severity separately improves realism

- Risk is nonlinear and concentrated in specific segments

- Random Forest captures interactions that linear models miss

- A small subset of customers drives a large share of total loss